Auto Added by WPeMatico

Long-term growth outlook remains intact, and market pullbacks may offer buying opportunities for quality assets

by IFAST RESEARCH TEAM

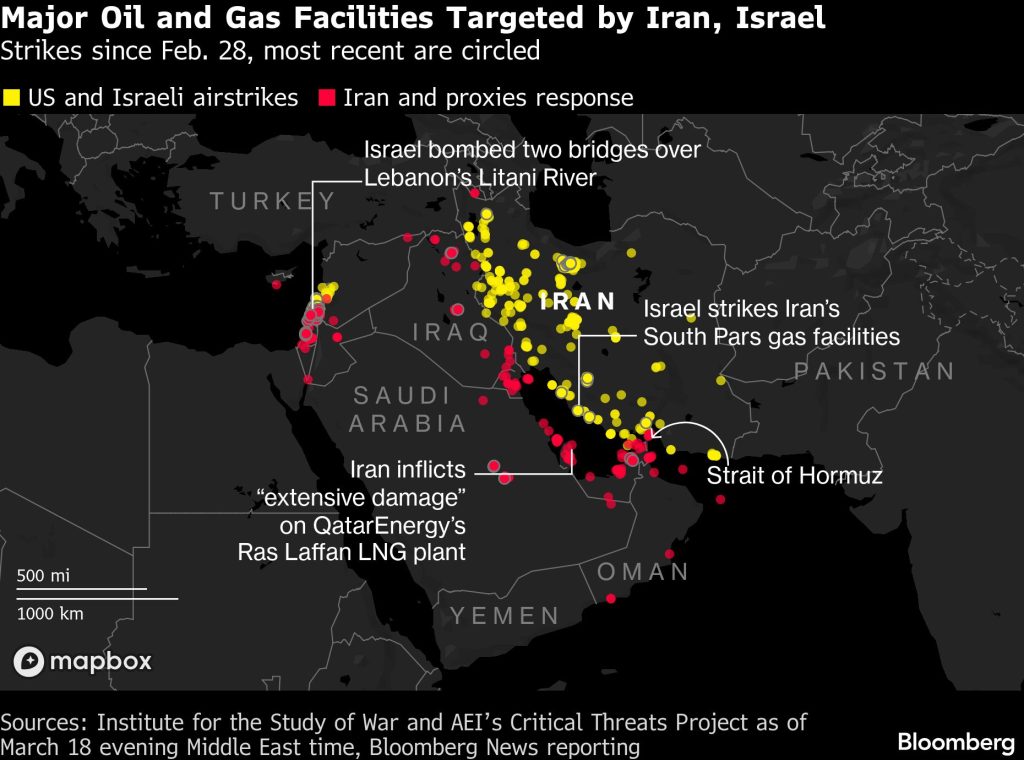

JOINT US-Israeli strikes on Iran that began on Feb 28 have jolted global markets into a fresh bout of geopolitical anxiety. The ensuing disruptions around the Strait of Hormuz — a chokepoint through which roughly 20% of global oil and gas (O&G) supplies pass — have heightened fears of prolonged energy supply shocks and pushed investors sharply into “riskoff” mode.

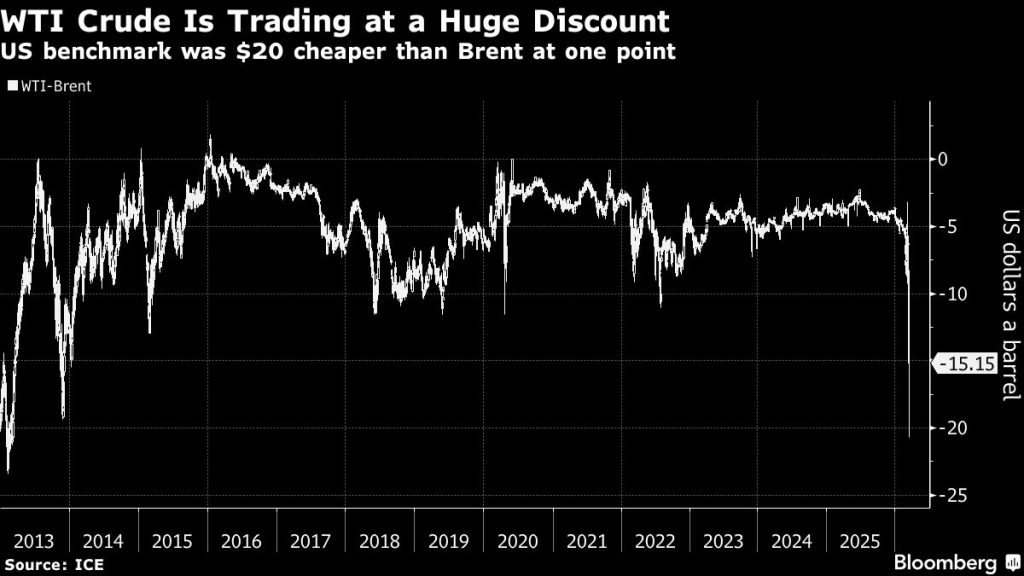

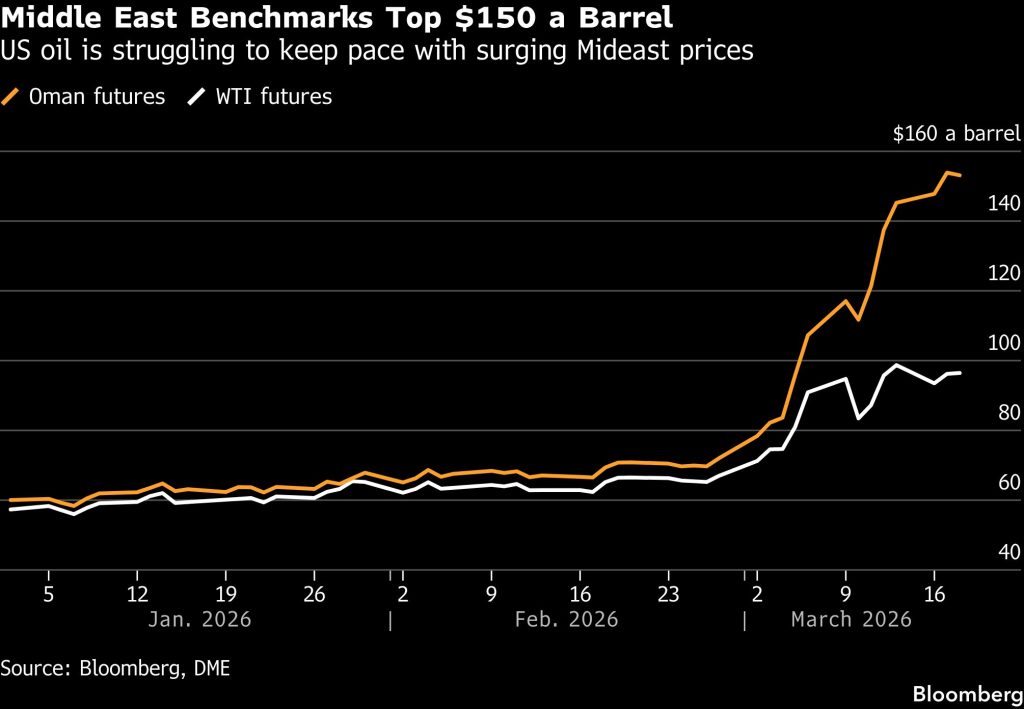

The immediate market reaction was swift. Brent crude surged over US$84 (RM330.12) per barrel, while shipping insurance premiums for vessels transiting the Persian Gulf reportedly quadrupled overnight. From Hong Kong’s trading floors to Seoul’s technology corridors, Asian equities reopened to a far more uncertain world.

Why do Asian Markets Feel the Burn?

Asian markets opened sharply lower at the start of last week, with broad-based selling across energy-dependent and technology-heavy indices.

The MSCI Asia ex-Japan Index has fallen -9.3% since the last trading day of February, reflecting a swift shift to risk aversion. Within the region, South Korea emerged as the epicentre of the sell-off.

The transmission mechanism from the Middle East conflict to Asian equities is a clear chain of economic causality.

The oil-inflation tax: Many of Asia’s largest economies are structurally reliant on imported energy, particularly from the Middle East. South Korea sources about 60%-70% of its crude oil from the region, Japan around 90%-95%, and India more than half.

When oil prices spike, it effectively acts as a tax on these economies. Higher crude oil costs raise manufacturing and transport expenses, squeeze corporate margins and push up consumer prices. From semiconductor fabs in South Korea to car manufacturing plants in Japan, input costs climb quickly when energy markets tighten.

The global easing narrative that dominated the start of the year becomes more complicated: An oil shock risks reigniting imported inflation, raising the possibilities that major central banks will keep rates “higher for longer”. Combined with lingering tariff pressures, inflation expectations could become sticky again.

As the probability of policy easing falls, equity valuations, particularly growth and technology stocks, face renewed downward pressure. In Japan, economic uncertainties have sharply reduced the likelihood of a March rate hike, leaving the Bank of Japan (BOJ) in a cautious “wait-and-see” stance.

Flight to safety: Geopolitical shocks trigger capital rotation out of high-valuation growth stocks into defensive and perceived safe havens and toward defence contractors and energy-linked names. Technology-heavy markets such as South Korea, Japan, Taiwan and Hong Kong are therefore particularly exposed.

Artificial intelligence (AI), software and semiconductor stocks, already trading on elevated expectations, are now facing sharper scrutiny. Concerns over the sustainability of capital expenditure (capex) and long-term demand growth amplify the risk of valuation resets.

Will This Situation Escalate or Fade?

There are reports that diplomatic backchannels may exist, though public rhetoric from both Washington and Tehran remains uncompromising. The trajectory of Asian equities will still depend heavily on whether energy supply routes remain disrupted and the conflict broadens regionally.

It is worth noting that prolonged disruption of the Strait of Hormuz would damage not just importers, but also exporters, including Iran itself. Sustained oil spikes are economically painful for the US, Israel and Gulf economies alike. Elevated costs putting pressure on both sides could raise the probability that this remains a contained, rather than systemic.

The Tactical Playbook

On March 5, Asian markets staged a rebound, with South Korea leading the recovery. The Korea Composite Stock Price Index (KOSPI) surged about 10% in a single session after President Yoon Suk-yeol announced a 100 trillion won (RM300 billion) market stabilisation fund, effectively placing a floor under the region’s worst-performing market. At the same time, stronger-than-expected US economic data, including private-sector hiring and services activity, signalling that the global economy may be resilient enough to absorb the recent oil shock. Together, these developments have helped restore some confidence in equity markets, even as the conflict in the Middle East continues to create uncertainty.

Our base case remains elevated volatility in the near term but no structural derailment of Asian growth. If this proves to be a shortlived geopolitical episode, current pullbacks may represent valuation resets rather than fundamental breakdowns.

In markets, panic often overshoots reality. For disciplined investors, periods of dislocation frequently sow the seeds of the next cycle of returns. The key is not to retreat, but to reposition intelligently.

Asian semiconductor hubs’ investment case remains intact. Demand for South Korean high-bandwidth memory (HBM) chips continues to grow, while global semiconductor capex is pausing for reassessment rather than entering a structural downturn. At the same time, defence spending is emerging as a second tailwind, with companies such as Hanwha Aerospace Co Ltd benefiting as governments strengthen security priorities. The recent sell-off, therefore, creates an attractive entry point.

Taiwan’s market correction has been relatively milder than South Korea’s, despite its similarly technology-heavy index. This resilience reflects the island’s more diversified energy mix and the dominant position of Taiwan Semiconductor Manufacturing Co Ltd (TSMC), whose near monopoly in advanced chip manufacturing and strong pricing power create a formidable moat around its valuation.

As the only foundry capable of producing two-nanometre chips at scale, Taiwan’s structural advantage in semiconductor manufacturing remains firmly intact for the foreseeable future. The recent pullback therefore presents a tactical opportunity for investors to add exposure.

China remains a major oil importer, but it is relatively better cushioned by its strategic petroleum reserves, policy flexibility and strong state influence over energy supply chains. Ongoing support from the annual “Two Sessions” continues to reinforce pro-growth measures, innovation funding and private-sector development.

While Hong Kong-listed technology stocks have faced sharper corrections due to their higher growth exposure, mainland A-shares have shown greater resilience, supported by domestic liquidity and policy backing. For long-term investors, the broad-based technology sell-off presents an opportunity to accumulate high-quality franchises at more attractive valuations.

Singapore continues to serve as a stabiliser within regional portfolios. The Straits Times Index is supported by its high concentration of dividend-paying banks, strong corporate balance sheets and its standing as a regional safe-haven financial hub. Improving liquidity and strengthening sentiment toward small-and mid-cap companies — aided by initiatives such as the Equity Market Development Programme — are also providing incremental support to valuations.

Meanwhile, within Malaysia, robust domestic economic fundamentals, improving corporate earnings and relatively inexpensive valuations continue to position the domestic equity market to attract potential foreign fund flows ahead.

With Asia’s structural growth drivers remaining firmly intact, we encourage investors to maintain a positive long-term view on the region and use market pullbacks as opportunities to accumulate quality assets at more attractive valuations.

Outside the Asia ex-Japan region, Japan’s growth story also remains intact. Its long-term investment case is not dependent on Middle East geopolitics. The corporate reform push is expected to continue to yield results in 2026. Corporate profitability is improving, governance standards are rising, and domestic stimulus under Prime Minister (PM) Sanae Takaichi’s era remains supportive. Short-term volatility does not erase multi-year structural change.

- The views expressed are of the research team and do not necessarily reflect the stand of the newspaper’s owners and editorial board.

- This article first appeared in The Malaysian Reserve weekly print edition

The post Middle East war rocks Asian markets, but don’t let fear drive your trades appeared first on The Malaysian Reserve.