Recent softness in profits appears more cyclical than structural, likely driven by a cautious pullback in biz investment

by IFAST RESEARCH TEAM

NIKKEI 225 staged a strong V-shaped recovery following its sharp dip on April 2, Liberation Day, yet, there is still a loss year-to-date (YTD) as the falling US dollar/Japanese yen pair, in large due to relative weakening of the US dollar and tariff-induced safe haven flow into the yen so far.

The Nikkei 225 (price-weighted) saw a steeper decline, while the cap-weighted Topix Index, especially large exporters (Topix 30) and small-cap stocks (Topix Small 500), shows a milder impact despite yen rallied YTD, suggesting the still solid fundamentals in the Japan market.

Has Japan taken the hit? We have yet to see a significant deterioration in growth momentum, with corporate earnings remaining resilient despite signs of moderation. The recent softness in profits appears more cyclical than structural, likely driven by a cautious pull-back in business investment as firms anticipate weaker demand and brace for potential tariff-related disruptions. As shown, operating profits in Japan’s manufacturing sector are normalising after an outsized contribution during the post-Covid-19 recovery.

While the absolute trend remains steady, the sector’s profit share is reverting toward its long-term average, signalling contin- ued earnings growth, albeit more tempered and increasingly priced for future external headwinds.

BOJ Sees Less Room to Manoeuvre

Markets are again showing signs of a “buy the rumour, sell the news” pattern.

The recent selloff sparked by tariff headlines and US President Donald Trump’s tweets appears to overshadow macro positives, driving volatility and limiting the Bank of Japan’s (BOJ) flexibility to act boldly. In this fragile environment, the central bank is likely to proceed cautiously, with a calculated approach to avoid spooking markets further.

Japan, though not the centre of the turbulence, has not been spared. Panic selling has dragged even fundamentally strong sectors like exporters and financials lower, pressured by the yen’s sharp gain and fears of forex translation losses.

We expect two more rate hikes this year and bring interest rate to 1%, having pushed back expectations to July from May due to renewed tariff risks that rattled the inflation outlook. While some on the street expect the next rate move only in January 2026, being sceptical that hiking amid fragile sentiment and surging food costs surging could risk a sharp yen rebound and hurt the export sector.

Macro data is not signalling urgency for rate hikes either. Headline inflation appears overstated, driven largely by a near doubling in rice prices since March last year amid tight supply. This has delayed the recovery in real wage growth, which could hardly turn positive in the near term until food cost pressures ease and government incentives help.

That said, inflation progress is encouraging. Consumer prices have passed the 3% mark, a positive development after being stuck in the upper 2% range for months. This shift was initially helped by the roll-back of government utility subsidies last June. However, with those subsidies now partially reinstated and energy prices weakening, inflationary pressures may ease again in the near term, offsetting partially the elevated food cost.

On the wage front, momentum has stalled moderately after February’s bonus payouts, as most corporates are playing it safe. Many are reluctant to boost base salaries or commit to productivity-enhancing investments, opting instead to adopt a wait-and-see stance.

1Q25 Earnings Look Steady

While we expect upbeat headline results for the first quarter, the visibility into the coming quarters remains unclear. With US tariff policies still in flux, the financial year 2025 (FY25) guidance will be a key focus.

Tariffs, US recession risks and yen strength all pose headwinds for overseas demand-driven sectors. As a result, we prefer domestic demand-focused names, which are more insulated from external shocks. Business conditions remain favourable for real estate, information and communications, trans- portation and logistics. Retail sentiment is rebounding. In manufacturing, confidence remains strong in heavy machinery, a sector often buffered by capex cycles and infrastructure projects.

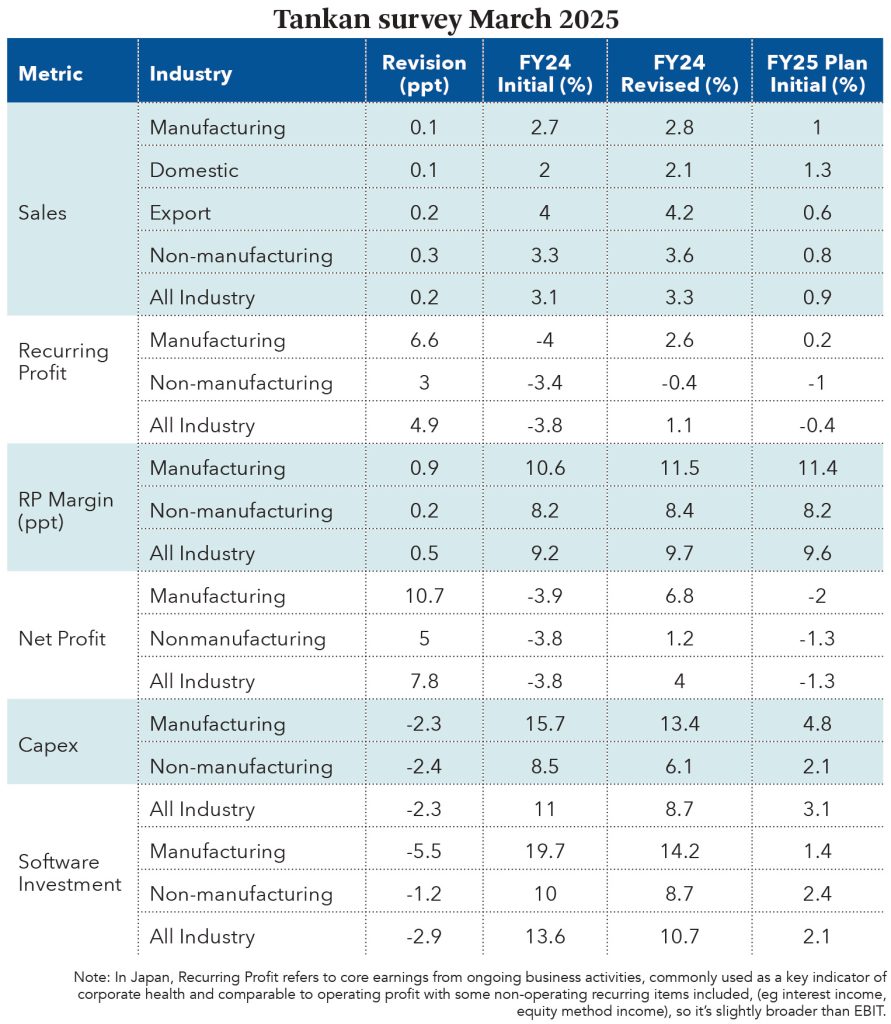

What the Tankan Survey Tells Us

The March 2025 BOJ Tankan survey offers a detailed snapshot of corporate sentiment. Sales expectations for FY25 slow to 1%, signalling caution amid global uncertainties. For recurring profit — a key metric in Japan akin to operating profit but slightly broader, where 2024 saw a significant upward revision from -4% to 2.6%, reflecting a surprising margin recovery. However, the 2025 plan flattens to just 0.2%, highlighting potential cost pressures and diminished pricing power.

Margins are improving for FY24 (10.6% to 11.5% in manufacturing), but may normalise slightly in 2025. Net profit growth for manufacturing in 2024 is now projected at 6.8%, outpacing non-manufacturing’s 1.2%. The green shoots in manufacturing suggest optimism that should tariffs ease, we may see further upward revisions that push FY25 growth into low single digits.

Capital expenditure (capex) trends, however, reflect lingering caution. After a -2.3% revision to 2024 plans, total investment is still strong at 13.4%, though that growth moderates to just 3.1% in FY25. Software investment, while still healthy this year, is forecast to decelerate sharply next year, hinting at front-loading of digital capex amid tariff-related uncertainty.

Impact of Stronger Yen on Japan Equities

We see the potential for US dollar/ Japanese yen to test the 135 level by end-2025, supported by persistent safe haven flows amid a dimmer trade and growth outlook, as well as ongoing geopolitical tensions. While we expect Japan to deliver two additional rate hikes, the moves are likely to be gradual and measured to avoid triggering a sharp unwinding of carry trades.

Assuming a conservative 5%-yen appreciation against the US dollar by end-2025 following a strong YTD gain of 10% to 142 (a simple back-test suggests a potential 14%), we estimate an earnings drag of -5.8% for the Nikkei 225. Roughly half of the pressure would come from the consumer discretionary sector (eg Toyota Motor Corp, Sony Group Corp, Fast Retailing Co Ltd, Honda Motor Co Ltd, Denso Corp) and the technology sector (eg Keyence Corp, Tokyo Electron Ltd, Fujitsu Ltd).

To clarify, we adopt the non-tax-adjusted EPS impact of -5.8% as a more prudent estimate that captures the broader downside risks from both macro headwinds and currency. Given the export-heavy nature of Japan’s equity benchmarks dominated by automakers, machinery and precision equipment, we believe that index earnings could suffer harder hit compounded by tariff-related pressures, slower global demand and sentiment-driven multiple compression. The higher-end estimate allows for a margin of safety in light of these layers of uncertainties.

Stay Bullish on Japanese Equities

Japan’s macro environment remains compelling for investors who are committed to long-term investing.

Small caps are worth another look, of which the United Japan Discovery Fund invests in domestic-oriented companies, hence less exposed to yen volatility and global trade shocks. In fact, small caps experienced shallower drawdowns during the recent selloff and could benefit from stable wage growth, resumed utility subsidies and soft energy prices, all of which support discretionary spending at home.

- The views expressed are of the research team and do not necessarily reflect the stand of the newspaper’s owners and editorial board.

- This article first appeared in The Malaysian Reserve weekly print edition

The post Time to relook at Japan appeared first on The Malaysian Reserve.