Data centre demand, infrastructure spending and foreign investments keep construction outlook steady despite global and policy risks

by IFAST RESEARCH TEAM

MALAYSIA’S construction sector has achieved a significant milestone in 2024, with the value of construction work done reaching RM158.8 billion, reflecting a robust growth of 20.2% year-on-year (YoY), contributed to the Bursa Construction Index (KLCON) 59.14% return. Such remarkable performance was primarily fuelled by substantial expansions in the special trade activities and residential building subsectors, driven by strong domestic economic growth, infrastructure development and the prosper development of data centres.

However, plot twisted as we enter 2025, the construction sector experienced a massive sell-off, mirroring the broader market downturn, largely driven by dampened sentiment due to the chip restrictions imposed by the Biden administration and ongoing global trade uncertainties.

Despite the selloff, there are no indications of a slowdown in the companies’ project pipelines and the earnings have remained intact. As such, we remain confident that the Malaysian construction sector is well-positioned for growth, driven by several key factors including the expanding orderbooks of construction companies, the ongoing domestic infrastructure projects, foreign project exposure, public-private partnerships (PPP) under the PIKAS 2030 Master Plan, and the increasing flow of foreign direct investments (FDIs).

Govt Expenditure Boosts Construction Sector

After a challenging period for the construction sector during the Covid-19 pandemic, government development expenditure in Malaysia has increased steadily in recent years, with a notable rise compared to historical average since 2023, which reflects the government’s ongoing commitment to infrastructure and economic development. In Budget 2025, the government expenditure continues keeping the pace on this upward trajectory, with Work Ministry’s projected construction spending of RM 200 billion in 2025 and to continue focus on the basic infrastructure projects such as roads, electricity and clean water that could drive long-term growth and benefitting people.

More Projects are Rolling Out

A major momentum stem from expanding infrastructure pipeline and a supportive macroeconomic environment. With nationwide project development initiatives accelerating, the constructure sector remains a crucial pillar for economic expansion, driven by large-scale infrastructure projects, private-sector investments and FDI inflows.

One of the key structural drivers remains urban connectivity and transport infrastructure, with major transit systems such as the Johor Bahru-Singapore Rapid Transit System (RTS) Link and the progress continuation of Penang Light Rail Transit (LRT) expansion forming the backbone of Malaysia’s mobility strategy.

Industrial and commercial construction continues to scale up, particularly in response to Malaysia’s positioning as a regional hub for high-value industries. The Johor-Singapore Special Economic Zone (JS-SEZ) stands out as a significant catalyst, which could potentially attract new investments in advanced manufacturing, logistics and digital infrastructures, aligning with the broader FDI-driven expansion seen across key industrial hubs.

Additionally, water infrastructure and flood mitigation are becoming key components of the industry’s project pipeline, which is evident from Gamuda’s recent securing of the Sungai Perak Raw Water Transfer Scheme (SPRWTS), a bulk water transfer and flood control project. We believe Gamuda Bhd’s involvement in water infrastructure development could mark the beginning of a broader wave of such projects, as the deputy prime

minister’s announcement in February 2025 that the Ministry of Energy Transition and Water Transformation will expedite flood mitigation efforts, with up to 35 out of 136 projects currently in the pre-implementation stage.

As such, we remain positive on these infrastructure upgrades, which are expected to be key priorities in the construction sector’s project pipeline moving forward.

Material Costs Remain Fairly Stable

The cost of construction materials remains at a relatively low and stable level currently, despite some fluctuations in recent months. Cement prices have stabilised lately following a surge in 2024, driven by rising material costs and increased demand from the ongoing domestic infrastructure development. This stabilisation provides a more predictable cost environment for contractors, especially in light of the strong pipeline of infrastructure projects expected to fuel demand in the near term.

On the other hand, steel prices have remained lower, largely due to the oversupply in the global steel market, which has been exacerbated by excessive dumping from China. As a result, steel prices have been well-contained, providing relief to construction companies that rely heavily on steel for large-scale infrastructure projects.

While we do anticipate that strong demand driven by upcoming projects may exert some upward pressure on material costs, we remain confident that the overall impact on the gross margins of construction companies will be minimal. This is largely due to the strong pricing power many contractors currently hold, thanks to robust order books and the ability to pass on some of the increased costs to clients. As such, we believe the increased material costs are expected to be manageable and will not significantly affect the sector profitability.

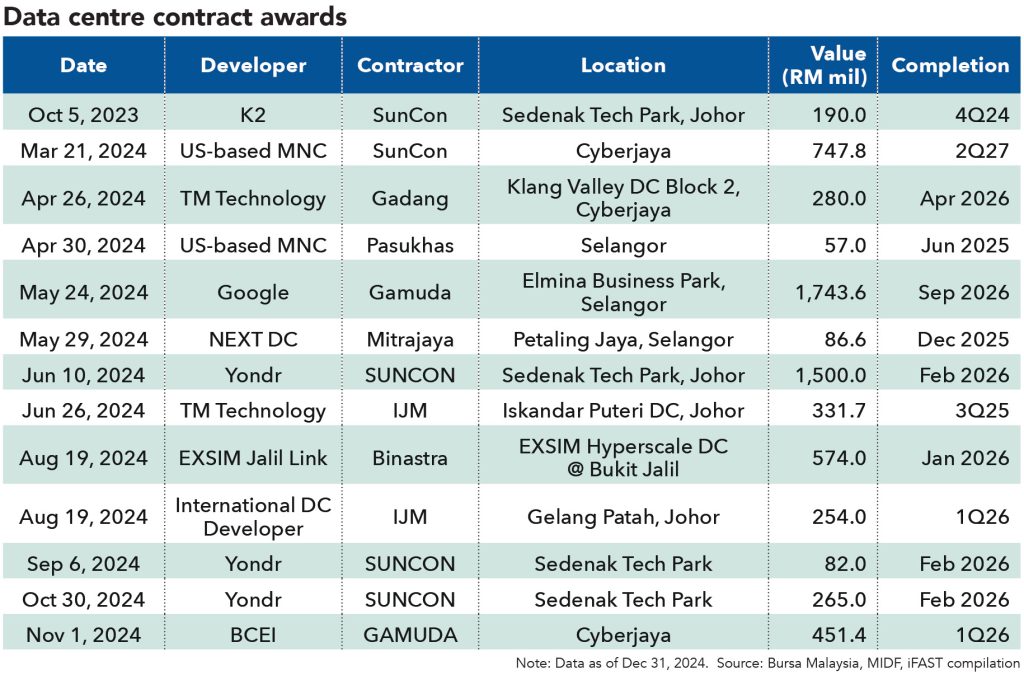

Data Centres Remain a Strong Catalyst

Furthermore, Malaysia’s data centre thematic play is another structural growth driver in the construction sector, capitalising on shifting regional dynamics and rising digital infrastructure demand. The lifting of Singapore’s four-year moratorium on data centres in early 2024 has positioned Malaysia as a prime alternative, with its competitive advantages of abundant power and water resources, cost-effective land, cheaper labour cost, and established infrastructure, making it a preferred destination for large-scale data centre investments. The increased reliance on artificial intelligence (AI) and high-performance computing that has further reinforced the demand for expanded data capacity, attracting significant investments from tech giants such as Google LLC, Amazon.com, and Microsoft Corp.

Despite the construction companies could directly benefitted from the data centres infrastructure demand, market sentiment took a hit following the implementation of US export restrictions on advanced computing integrated circuits (ICs) in January 2025. This move, particularly the imposed 50,000-chip annual cap for Malaysia as a tier 2 country, led to short-term volatility, weighing on construction stocks.

That said, we believe the concerns appear overstated, as most data centres in Malaysia are cloud-based, rather than AI-powered large language model (LLM) processing, which therefore do not require advanced graphic processing graphics processing units (GPU) chips, and the impact of these restrictions is likely to be smaller.

Looking ahead, we believe the Malaysia’s data centre play remains intact as the pipeline for new data centre developments continues to expand, providing substantial opportunities for construction players with exposure to this theme. Companies such as Sunway Construction Group Bhd (SunCon) and IJM Corp Bhd, which have already secured a few data centre contracts, are well-positioned to capitalise on this structural trend. With rising digital infrastructure investments, and continued government commitment to digitalisation, we believe Malaysia’s role as one of the key data centre hubs is set to strengthen, benefitting the construction sector’s growth potential despite near-term volatility.

The Downside Risks from Recent Govt Policies Exist

As the construction sector is inherently labour-intensive, we acknowledge certain downside risks, such as the minimum wage hike to RM1,700 introduced in Budget 2025 and the mandatory 2% EPF contribution for foreign labour.

Notably, Gamuda, SunCon and IJM, the three largest construction companies in the KLCON has already compensated most of their construction workers above RM1,700, this would limit the direct impact from the wage hike. Additionally, the median wage in the construction sector has consistently remained above RM2,500, suggesting that the impact on larger construction firms will be minimal.

However, smaller construction firms that currently pay wages below RM1,700 may face cost pressures. Similarly, the mandatory 2% EPF contribution for foreign workers, set to take effect in Q4 2025, is also expected to affect the construction companies’ earnings.

Key Takeaway

Gamuda, IJM and Sunway Construction are having bright prospects that have secured a substantial amount of infrastructure projects in their orderbook, subsequently supporting the future earnings.

- The views expressed are of the research team and do not necessarily reflect the stand of the newspaper’s owners and editorial board.

- This article first appeared in The Malaysian Reserve weekly print edition

RELATED ARTICLES

Healthcare 2025: Immunise your portfolio for next growth wave

The worst is over! The global financials sector prepares for increased certainties

Bumpy road ahead for construction sector

Vietnam: Brighter days ahead after a challenging year

Endemic phase heralds favourable macro environment and earnings prospects

Will the stock market roar in the Year of Dragon?

The post Malaysia’s construction outlook 2025 appeared first on The Malaysian Reserve.