by AUFA MARDHIAH & AZALEA AZUAR

LEMBAGA Tabung Haji (TH), the country’s pilgrimage fund, is urged to undertake structural reforms to protect depositors and return to its founding purpose.

Among the measures proposed are capping large deposits, tightening oversight and scaling back the fund’s risk-appetite especially on high capital investments.

Calls were made in reference to TH’s 2018 crisis, largely due to political interference and false dividend pay-out which subsequently forced the government to inject funds totalling RM19.9 billion to restore its balance sheet.

Although the fund has since stabilised, stakeholders and observers are pushing for deeper structural changes to prevent a repeat of past mistakes. Reforms must go further to safeguard TH’s long-term integrity.

Established in 1963 to assist Malaysian Muslims in saving for haj through Shariah-compliant means, TH has grown into a major fund institution, managing over RM90 billion in assets from nearly 9.5 million depositors.

Recommendations on the Table

One of the most discussed recommendations is to limit the amount that any individual can deposit in TH. Currently, there is no cap, allowing affluent individuals to use the fund as a secure, high-return savings vehicle backed by a full government guarantee — a benefit not extended to ordinary bank accounts.

In 2021, this guarantee covered RM83.3 billion of deposits — the highest in TH’s history — raising concerns that the fund is being used for wealth accumulation than for its intended purpose of pilgrimage savings. Reform advocates argue this practice distorts TH’s social mission and disproportionately benefits the rich.

Economist Dr Nungsari Ahmad Radhi believes that those who have performed the haj should not be allowed to keep large deposits in TH accounts.

“People should not have millions in their TH account and expect to be paid good dividends.

“Maybe those who have gone to haj should not be allowed to have more than a certain amount in their accounts,” he told The Malaysian Reserve (TMR).

There is currently no limit on how much depositors can save in TH, although the idea of imposing a cap has already been discussed at the policy level.

Daily cash withdrawals are limited to RM10,000, while larger amounts can be transferred to local bank accounts via telegraphic transfer at any TH branc

For now, daily cash withdrawals are limited to RM10,000, while larger amounts can be transferred to local bank accounts via telegraphic transfer at any TH branch.

The no-deposit-limit policy have been attributed as one of the many reasons inducing the fund to take up a high-risk investment appetite.

In 2018, the government disclosed that TH had been paying bonuses (hibah) erroneously since 2014, despite liabilities exceeding assets by RM4.1 billion.

Among the contributing factors were over-valued land acquisitions — such as a controversial RM188.5 million deal involving 1Malaysia Development Bhd (1MDB) — and creative accounting practices that was forcing payouts ahead of elections.

To rescue TH, the government trans- ferred RM9.6 billion worth of underperforming assets to a special-purpose vehicle, Urusharta Jamaah Sdn Bhd (UJSB), in exchange for RM19.9 billion comprising sukuk and cash. This move aimed to restore TH’s balance sheet and safeguard public confidence.

However, UJSB later reported a net loss of RM9.95 billion for the financial period ending Dec 31, 2019 (FY19), primarily due to impairment charges from the acquired assets.

Since then, however, TH’s finances have improved.

Last March, TH declared a 3.25% dividend for FY24 — the highest in seven years — benefiting over 9.54 million depositors with a total payout of RM2.92 billion.

As of Dec 31, 2024, its total assets under management stood at RM95.06 billion, surpassing its deposit liabilities of RM91.75 billion.

Sha

Sha

From Investing to Facilitating

Another point under consideration is whether TH should shift its focus from investments to its original mandate of facilitating the haj pilgrimage.

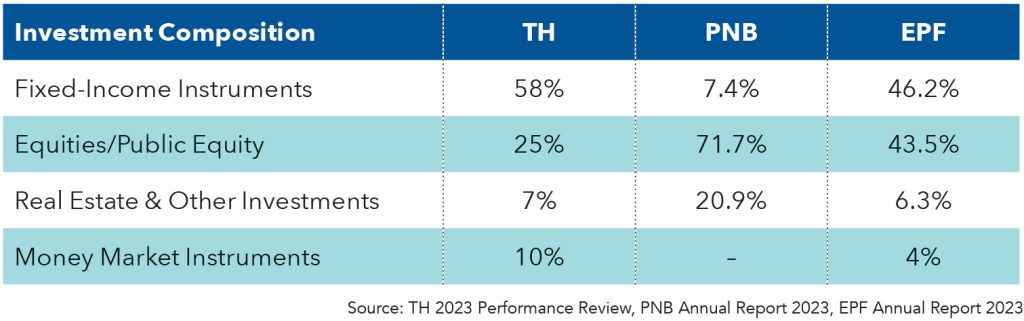

International Islamic University of Malaysia’s (IIUM) Institute of Islamic Banking and Finance assistant professor Dr Nazrul Hazizi Noordin said while TH has faced controversies over certain investment decisions, the current risk level is relatively low.

“TH already maintains a relatively low exposure to high-risk assets compared to other Malaysian investment institutions such as Permodalan Nasional Bhd (PNB) and the Employees Provident Fund (EPF),” he told TMR.

For FY24, 57% of TH’s investment income is derived from fixed-income instruments, 27% from equities and the rest from other sources — a conservative structure aligned with its haj savings mission.

Nazrul Hazizi also emphasised the importance of robust governance measures, calling for clear exposure limits, regular portfolio reviews and enterprise-wide risk manage- ment to prevent future mismanagement and political interference.

He added that TH operations still reflect its religious and social mandate. In 2024, the fund paid RM99.35 million in zakat on behalf of its depositors, benefitting over 670,000 asnaf.

Additionally, TH contributes to social causes such as poverty eradication and healthcare.

Nazrul Hazizi proposes for TH to explore a hybrid model by incorporating waqf to support operational haj costs for lower-income pilgrims (pic: TMR)

Referring to TH’s daily withdrawal cap, Nazrul Hazizi said that “these limits are designed to preserve the savings of depositors, ensuring that their funds remain intact and available when the time comes for them to perform haj.”

He also proposed that TH explore a hybrid model by incorporating waqf to support operational haj costs for lower-income pilgrims. This, he said, would also reduce the pressure on TH’s investment fund while preserving its affordability mission.

On the other hand, Nungsari questioned whether TH’s dual role — managing both savings and haj operations — should remain under one roof.

He further highlighted TH’s dual role with each function requiring different competencies and regulatory oversight.

“As it is, both reside in the same institution. That is a major weakness, in my view,” he said.

At the same time, Nungsari proposed that TH’s deposit-taking functions be regulated by Bank Negara Malaysia (BNM), while its fund management activities should be put overseen by the Securities Commission (SC). Alternatively, both functions could be outsourced entirely, allowing TH to concentrate solely on managing haj operations for a fee.

Those who have gone to haj should not be allowed to have more than a certain amount in their accounts, opines Nungsari (pic: TMR)

TH’s governance has also come under scrutiny, especially following past political appointments and allegations of mismanagement. Historically, TH has been put under the Minister in the Prime Minister’s Department (Religious Affairs), with its board membership are often politically appointments.

To address this, the government announced in 2021 that TH would be listed as a “prescribed Islamic financial institution” under Section 223 of the Islamic Financial Services Act 2013. bringing it under BNM’s oversight. This move places TH under the regulatory purview of BNM, aiming to enhance financial discipline and implement higher standards of risk management.

Nungsari said TH’s size alone makes it a potential systemic risk.

“An insolvent TH is a risk to the financial system. It is some RM95 billion in size. In 2018, it became necessary for the government to bail out TH because its assets were less than its liabilities.”

While some critics worry that BNM’s involvement may undermine TH’s religious mission, Nungsari disagrees.

“What social role does TH play? I do not see it playing a ‘social role’; it is a savings institution that manages the haj pilgrims.”

If TH retains its current structure, it should be subjected to comprehensive regulation across all its activities.

He also advocated for redefining TH’s corporate status. While often grouped with government-linked companies (GLCs), TH is distinct in that it manages private deposits for a religious purpose.

TH was established in 1963 to assist Malaysian Muslims in saving for haj through Shariah-compliant means (pic: MEDIA MULIA)

Treating TH as a GLC opens the door to political interference and pressure to support government-linked investments.

Removing TH from the GLC framework could reinforce its duty to depositors over government interests, he added.

Professionalising its board, removing political appointees and strengthening fiduciary responsibilities are also key parts of any reforms.

Since 2019, TH has brought in banking professionals and followed internal recommendations from the Royal Commission of Inquiry (RCI), whose findings remain classified.

In February 2025, Religious Affairs Minister Datuk Dr Mohd Na’im Mokhtar informed Parliament that TH is in the final stages of reclaiming assets from UJSB.

TH’s deposit-taking functions was proposed to be regulated by BNM

The process is expected to be “orderly” and have no financial impact on depositors, suggesting that TH has improved its governance to manage these assets again.

To sum it up, TH has made significant progress since its financial debacle, but the path forward depends on whether reforms can address its structural weaknesses.

Capping large deposits would reduce systemic risk and restore TH’s social mission. Refocusing on pilgrimage services over profit-making ensures it remains a fund for the people, not for the wealthy.

Moreover, enhancing governance — including tighter oversight and possibly redefining TH’s institutional identity — could make it resilient against future political and financial misuse.

For now, the institution remains a vital tool for Malaysian Muslims but to protect it, policymakers will need to balance trust, transparency, and TH’s core Islamic purpose — all while ensuring it remains sustainable for generations to come.

- This article first appeared in The Malaysian Reserve weekly print edition

The post Returning Tabung Haji to purpose appeared first on The Malaysian Reserve.