MALAYSIA’S monetary policy outlook is increasingly shifting into dovish territory, with economists now flagging the growing possibility of a rate cut as early as the second half of 2025 (2H25) — a notable acceleration from previous forecasts.

“Given the significant weakening in domestic growth momentum and rising downside risks, the case for an earlier OPR cut has increased,” said RHB Investment Bank Bhd (RHB Research) in a recent note.

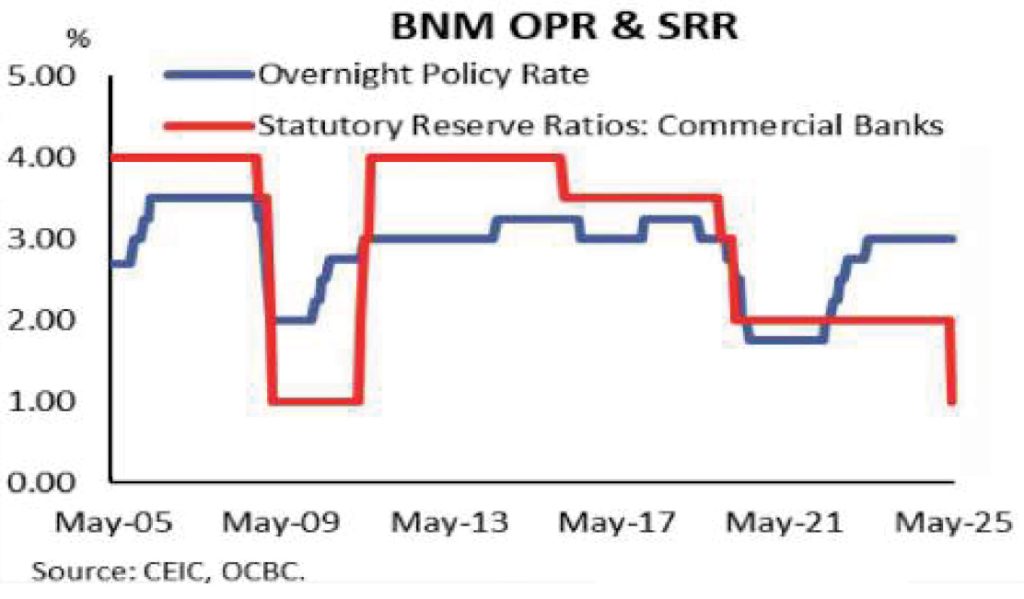

While RHB Research maintains its base case for the Overnight Policy Rate (OPR) to remain unchanged at 3% this year, it now sees a “balance of risk” for a potential 25 basis points (bps) cut in 2H25 if GDP growth dips below the critical 4% mark.

Oversea-Chinese Banking Corp Ltd’s (OCBC Bank) Global Markets Research shares this cautious view, albeit with a slightly more delayed base case. “Our baseline is for a cumulative 50bps in rate cuts in 1H26, but there is a clear risk that the rate cut could be brought forward to 2H25,” the bank stated in its own post-Monetary Policy Committee (MPC) analysis.

OCBC Bank also highlighted that Bank Negara Malaysia (BNM) has taken a more dovish tone, recognising “downside risks in the economic environment” and noting that the “balance of risks to the growth outlook is tilted to the downside”.

Both RHB Research and OCBC Bank point to BNM’s subtle but notable shift in language during its May MPC meeting.

The central bank dropped its previous assurance that the current policy stance “remains supportive of the economy” — a telling omission that suggests increased sensitivity to weakening macroeconomic conditions.

In a further signal of accommodative intent, BNM also announced a surprise 100bps cut to the Statutory Reserve Requirement (SRR), bringing it down to 2% effective May 16.

OCBC Bank noted that although BNM stated the SRR cut is not a signal of policy stance, “SRR cuts have more often than not been precursors to OPR cuts,” citing the pattern seen in 2019-2020.

Growth headwinds are mounting. RHB Research revised Malaysia’s 2025 GDP growth forecast down to 4.5% from 5%, warning that the figure could slip to as low as 3.5% if trade tensions escalate further.

Despite resilience in household consumption, weaknesses in fixed investment and public spending are increasingly weighing on economic momentum.

According to OCBC Bank, while the first quarter of 2025 (1Q25) GDP growth is expected to come in at around 4.4%, the composition of growth is concerning — driven largely by a volatile rebound in mining output, while manufacturing and electricity production remain weak.

BNM itself acknowledged that the external environment remains fraught with “considerable uncertainties”, including the outcomes of global trade negotiations and persistent geopolitical tensions.

This uncertainty has been compounded by mixed signals from industrial production data and a deterioration in global trade conditions.

On inflation, both research houses see price pressures remaining subdued.

RHB Research estimated headline inflation to average around 2.2% in 2025, potentially slipping to 1.6%-1.8% if domestic demand continues to soften.

OCBC Bank observed that BNM’s latest statement removed references to “upside” inflation risks, suggesting a more balanced inflation risk profile — potentially giving BNM more leeway for easing.

On the foreign exchange (forex) front, the ringgit is expected to remain sensitive to external developments. RHB Research maintains a year-end US dollar/ringgit forecast of 4.20-4.30, citing narrowing US-Malaysia real rate differentials and ongoing fiscal reforms as partial buffers. However, both institutions acknowledge that volatility may persist, especially amid rising global policy uncertainty.

For now, BNM appears to be treading carefully — keeping policy steady while quietly preparing the ground for a potential rate cut if economic data deteriorates further.

While neither RHB Research nor OCBC Bank anticipates an imminent move, both are now explicitly warning that a cut in 2H25 is no longer just a tail risk — it is an increasingly plausible scenario. — TMR

- This article first appeared in The Malaysian Reserve weekly print edition

The post Rate cut could come sooner as BNM turns dovish appeared first on The Malaysian Reserve.